Private equity and venture capital firms, direct lenders, investment banks, and other private markets firms execute many non-disclosure agreements (NDAs) each year. How they handle those contracts can differ considerably. Some require their in-house business professionals to handle NDA negotiations, which can be a new and intimidating prospect for a junior analyst or associate.

This article is intended to help business professionals without a legal background become more familiar with NDAs should these contracts come across their desks.

What is an NDA?

An NDA is a binding contract between at least two parties stating that one or more parties will keep the information disclosed to them confidential. It is often a standalone contract; however, parties can also include a confidentiality provision within a broader agreement.

Alternative asset managers, such as private equity firms and investment banks, sign transactional NDAs with other parties to ensure business information remains confidential during due diligence of a potential investment, merger, acquisition, sale, or financing transaction.

What is an NDA used for?

Generally speaking, individuals, businesses, and other entities use non-disclosure agreements to protect their sensitive information when they disclose it to other parties.

Common scenarios that often call for NDAs include:

- Employment relationships: Employees often have access to proprietary business information that should remain secret from the public and competitors. Employment NDAs are common for tech companies, startups, marketing agencies, and manufacturers.

- Product licensing: Companies that sell or license products and technology want to protect their data from being used or disclosed by third parties.

- Client relationships: Businesses and professionals may give clients sensitive information during their relationship, and an NDA requires those clients to keep that information secret. Conversely, businesses also generally agree to keep their clients’ information confidential either through an NDA or as a matter of professional duty.

- Prospective investors: Businesses typically disclose critical information to potential investors and require those investors not to disclose the information.

- Inventions: Inventors often use confidentiality agreements to protect their intellectual property before they can apply for and receive patents.

- Settlements: Some companies might insist on an NDA to protect the terms of a settlement reached through litigation or arbitration.

- Business transformations: Companies will often enter into NDAs when they are contemplating an acquisition of assets, a merger or business combination, or a major financing event.

NDAs for private equity, venture capital, and private credit

For alternative asset managers, such as private equity and venture capital firms, direct lenders, and advisors like investment banks, NDAs are routine contracts entered into at the beginning of discussions about or evaluation of potential transactions. Firms enter into hundreds or thousands of these agreements each year in order to receive or disclose sensitive business information and facilitate due diligence on potential acquisition, investment, merger, sale, or financing transactions.

Private equity NDAs are entered into by a buyer — usually a private equity fund — and a seller — usually an investment bank or a target company — to evaluate an investment in or purchase of assets from a target company.

Transactional NDAs in the private markets are primarily one-way, with the buyer or private equity firm receiving information from an investment bank or target company agreeing to keep the target company’s information confidential. However, many transactional NDAs will also require the investment bank or target company to keep the buyer’s name or interest in the transaction confidential.

Mutual NDAs are more common when a transaction involves a business combination or merger of two companies or when the target company must perform substantial diligence on the buyer.

Buy-side vs. sell-side

When people refer to “buy side” NDAs, they usually mean the process of reviewing and negotiating a confidentiality agreement by or on behalf of a private equity buyer. When people refer to “sell side” NDAs, they usually mean the process of reviewing and negotiating an NDA by an investment bank or on behalf of a target company. Typically, only one agreement exists, but depending on whether you are negotiating on behalf of a buyer or seller, you may refer to the same NDA as “buy side” or “sell side,” depending on your perspective.

The larger the private fund, asset manager, investor, bank, or adviser, the more NDAs they negotiate. A high volume often burdens large organizations because everyone involved wants to execute each agreement within days, not weeks. To achieve shorter turnaround times, businesses either need adequate internal resources, an NDA outsourcing provider, or a SaaS solution.

Who is the receiving party?

In a typical transactional NDA, an alternative asset manager, such as a private equity, venture capital, direct lending, or financing firm, is the potential buyer, investor, or lender and is the receiving party that receives information about a target company.

Who is the disclosing party?

In a typical transactional NDA, an investment bank acting on behalf of a target company or the target company itself is the potential seller or borrower and the disclosing party that discloses information about the target company.

Guide: How to draft an NDA

The information being disclosed and the representations & warranties, covenants, and obligations that parties want to include in an NDA depend heavily on their industry and intent.

Private equity firms, alternative asset managers, and investment banks use NDAs during private equity and private markets investment, business combination, and financing transactions. They often include terms other industries wouldn’t.

Businesses learning how to write an NDA should begin by connecting with their in-house legal team to understand the agreement’s purpose and the business’s preferred and fallback positions. Some will have a contract playbook to base markups and negotiations on. If not, the in-house legal team may be able to provide an NDA template or a previously executed NDA.

Terms confidentiality agreements should include:

The parties to the contract

There must be at least two parties, and the NDA should define who will provide and who will receive confidential information.

The purpose

The NDA should identify the purpose of the exchange of information, such as a business combination, evaluating software or services, or protecting information disclosed during the course of employment.

The definition of confidential information

The NDA should define what information is covered by the agreement and will be subject to its obligations. Parties should be specific about what types of information they consider confidential. Definitions that are overly broad may be difficult to enforce, while definitions that are too narrow may not sufficiently protect the parties.

The obligation not to disclose confidential information

The NDA should include an explicit covenant to protect and not disclose confidential information. It may set forth certain steps or processes that must be undertaken in connection with that protection.

Permitted use of confidential information

Generally, the NDA should clarify to whom confidential information may be disclosed and for what purposes it is permitted to be used. For example, in transactional NDAs, recipients may need to disclose information to advisors or financing sources or use information to conduct diligence or secure co-investment.

The degree of care

Generally, an NDA will provide that a recipient must use at least reasonable care to protect another party’s confidential information. Some NDAs may specify a higher degree of care. Terms like “best efforts,” “reasonable,” or “commercially reasonable” are legal standards generally defined by common law and precedent and may vary significantly depending on the governing law of the agreement.

The duration of the agreement

An NDA should generally have a fixed term and be clear about how long the contract and the obligations within it remain in force.

Tail or survival periods

If portions of the NDA are intended to remain in force or “survive” the term of the NDA, applicable terms and tail periods should be clearly defined.

Return or destruction of confidential information

Most NDAs contain provisions indicating what happens to confidential information after the purpose of the exchange is complete or after the term of the NDA has expired. Parties may agree to return or destroy confidential information but may need to retain certain types of information on a limited basis for compliance purposes.

Governing law/jurisdiction

A governing law provision indicates which country’s or state’s law will be used to interpret the terms of an agreement by a court or arbitrator. Jurisdiction refers to where claims may be brought.

Dispute resolution

Some NDAs may specify that claims will be brought via alternative dispute resolution mechanisms, like mediation or arbitration. In the absence of special provisions, most NDA disputes are resolved through litigation, which may include seeking injunctive relief.

Damages

NDA disputes are typically resolved through litigation, and courts will determine whether a breach occurred or whether damages are recoverable by applying governing contract law. In some cases, an NDA may provide that a party is required to indemnify another party for direct or third-party claims arising from an unauthorized use or disclosure of confidential information. Parties should pay particular attention to the inclusion of special, consequential, or indirect damages.

Signatures

An authorized representative of each party should execute the agreement.

Common private equity NDA provisions

Non-disclosure agreements for private equity investing or financing transactions may also include particular terms and provisions, including:

Definition of “Representatives”

Identifies the parties to whom the buyer may provide confidential information in connection with evaluating or financing a potential transaction.

Joinders

Buyers may require their representatives, particularly debt and equity financing sources, to sign a joinder in which the representative agrees to comply with the terms of the NDA between the buyer and seller.

Financing “Lock-ups”

Sellers may permit buyers to contact debt or equity financing sources but restrict a buyer’s ability to enter into exclusive arrangements or “lock-ups” that could limit the ability of those financing sources to provide financing to another buyer.

No-contact clauses

Sellers may restrict buyers’ ability to contact parties that have a relationship with the target company, including the target company’s employees, officers, directors, customers, suppliers, contractors, lenders, or other business relationships.

Non-solicitation

Many sellers include non-solicitation provisions that limit the buyers’ (and, in some cases, their portfolio companies’ or affiliates’) ability to solicit or hire a target company’s employees.

Standstills

When a target company issues public debt or equity, sellers may include a standstill provision that restricts potential buyers from trading in an issuer’s securities for some period of time.

When marking up or negotiating these and other terms, a business professional needs a strong grasp of the firm’s risk profile, preferred and fallback terms, and market norms. Without this information, the analyst or associate can introduce unnecessary risk for their firm, delay the execution of NDAs, or set a poor tone for a future business relationship.

Learn more about these and other industry-specific terms in Ontra’s guide to the Top 10 Private Equity NDA Terms.

How long is an NDA applicable?

A confidentiality agreement lasts until its term expires or is otherwise terminated. As noted above, some provisions may survive the termination of the agreement. A term of one to five years is common, but there is significant variance across industries.

In the private markets, a term of one to three years is customary, though certain circumstances may warrant a longer duration.

What happens if someone breaches an NDA?

The consequences of a breach of contract may range from a breakdown in a business relationship to litigation or legal action that results in monetary damages.

Sometimes, a disclosing party pursues legal action, such as suing the party responsible for the breach or initiating injunctive relief procedures. If the disclosing party can establish the recipient party’s breach of contract and damages, the court may order the breaching party to pay a certain sum of money or may enjoin it from taking a particular action. Disputes regarding NDA breaches may also be settled, including through the use of alternative dispute resolution.

A disclosing party might also have other causes of action under contract law or tort law, such as the right to sue based on trade secret misappropriation, unfair competition, or copyright infringement.

Quantifying damages for the breach of an NDA can be difficult. As a result, some parties may choose to define the damages a party is entitled to if the other party breaches the NDA by setting a total amount or providing a formula. A damages clause typically influences the settlement or court award.

Can someone under an NDA share information with advisors?

Whether a receiving party can share confidential information with anyone else, such as a vendor or advisor, depends on the text of the NDA. In the private markets, receiving parties typically carve out the right to provide confidential information to advisors and financing sources to conduct diligence on and complete potential transactions.

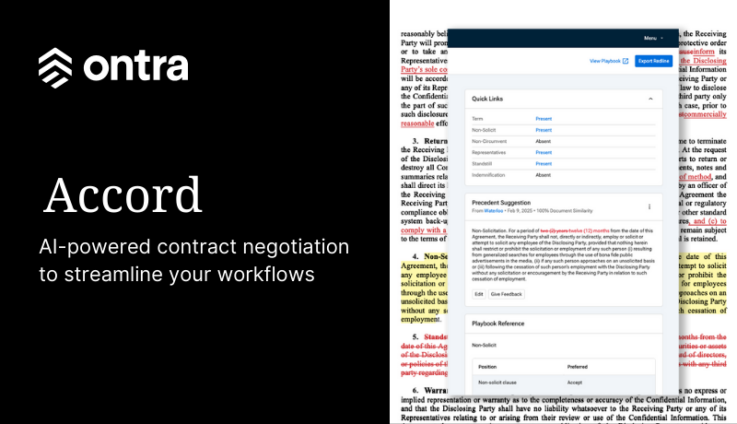

Ontra: The winning solution for high-volume contracts

Ontra’s AI-powered negotiation solutions accelerate and standardize agreements through automated clause analysis, streamlined redlining, and real-time insights for faster, more precise, and confident deal execution. Contract Automation fully takes repetitive agreements off firms’ hands, while Accord provides AI-powered negotiations to in-house teams.

Our negotiation solutions offer:

- Digital Playbooks: Standardize negotiation strategies for consistency and compliance.

- Markup Builder: Automate the redlining process with suggested markups to avoid starting each review from scratch.

- Similar Documents: Rapidly search and leverage relevant past NDAs to benchmark and align new agreements based on precedent.

- Summaries: Summarize key contract terms for informed, confident decision-making and faster approvals.

- Reports: Track aggregated insights on contract negotiations to unlock trends.

- Playbook Alignment Reports: Quickly reference a report to monitor adherence to the contract playbook at various stages of negotiation.

Interested in streamlining or automating your NDA negotiations? Schedule a Contract Automation demo or Accord demo today.