The volume of due diligence questionnaires only continues to climb. One GP told Ontra that the finance team handled 1700+ pages of questions from 70+ LPs during its latest raise. The principal even joked about wanting to cry when the first DDQ came in due to its length and complexity. The firm’s manual DDQ process was not scalable, relied on manual search, and faced significant challenges when answering new questions, especially during the tight fundraising timeline. The team had no choice but to “brute force” their way through.

- Fund managers are continually seeking new sources of capital,

- More retail investors are allocating to alternatives, widening the LP pool, and

- LPs are requesting more detail, making each DDQ longer and more complex.

All of these factors are prompting private equity firms to reevaluate their DDQ best practices.

Managing the increasing volume well means firms can’t treat every DDQ as a fresh project. It requires a continuous response program with a well-maintained answer library, clear ownership, and purpose-built AI that works across all DDQ types. With that kind of automated process, GPs can respond quickly and comprehensively to stand out from the competition, freeing their investor relations team for higher-value investor conversations.

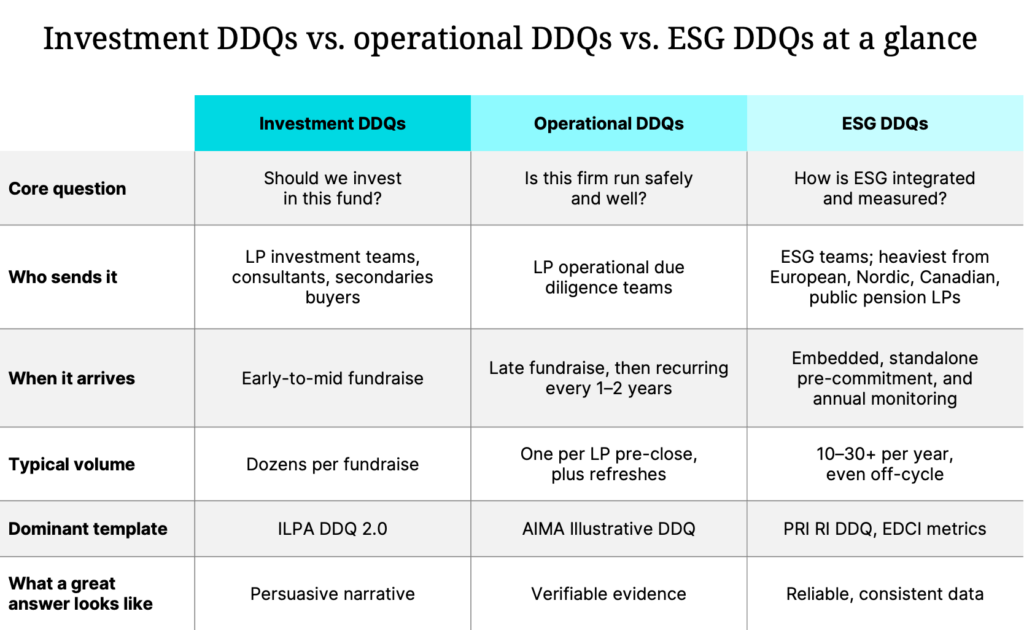

Investment DDQs vs. operational DDQs vs. ESG DDQs at a glance

3 types of DDQs private equity firms receive

Most DDQs fall into one of three categories: investment DDQs during fundraising, operational DDQs, and ESG DDQs. They share a common core, but each is sent on a different schedule, looking for different answers.

What is a fundraising or investment DDQ?

The workhorse. It arrives whenever the firm is fundraising, usually after a first or second meeting with an investor. The investor moves into formal diligence with a DDQ that covers strategy, track record, team, fund terms and economics, conflicts, and co-investment policy. Most run roughly 150 to 300 questions, and DDQs from large investors can exceed 400 once cybersecurity, ESG, and compliance sections are layered in. One GP told Ontra its team has filled out thousands of DDQs and addressed tens of thousands of questions across its fundraises.

The dominant template is the ILPA DDQ. The current version, ILPA DDQ 2.0, was released in 2021 and expanded from 8 to 21 sections. Most LPs use it as a chassis and bolt on proprietary questions. A pure, unmodified ILPA document is rare.

What is an operational DDQ (ODD)?

Sent by the LP’s operational due diligence team (usually separate from the investment team) late in a fundraise, then recurring every one to two years. An ODD examines how the firm runs: valuation policy, cash controls, compliance, cybersecurity, business continuity, service providers, and technology. A GP told Ontra it currently manages approximately 20 annual and 5-10 quarterly operational DDQs. The dominant template is AIMA’s Illustrative Questionnaire, first published in 1997 and now the industry-standard ODD template. The 2025 edition is modular and, for the first time, covers private equity and private credit alongside hedge funds.

What is an ESG DDQ?

Sent by investors to assess how a GP identifies, manages, and reports on environmental, social, and governance risks and practices. It can appear in three forms: embedded in a fundraising DDQ, as a standalone pre-commitment questionnaire, and as recurring annual monitoring, so even a firm not in market may field 10 to 30 per year.

The foundational framework is the PRI’s Limited Partners’ Responsible Investment DDQ; the ESG section of the ILPA DDQ 2.0 draws directly on it, and the two are deliberately synchronized. A 2025 PRI Climate Module, developed with ILPA and iCI, adds a focused set of climate questions, while the ESG Data Convergence Initiative standardizes the metrics many LPs ask GPs to report.

DDQ best practices that apply to every questionnaire

All three DDQ types share a substantial core list of questions: firm ownership and AUM, team and turnover, compliance and regulatory history, service providers, and conflicts. A large share of any incoming DDQ can be answered from previously approved language, which is why a searchable master library is the single biggest efficiency lever.

These six best practices apply no matter which type lands in the inbox:

- Maintain a master answer library. Centralize pre-approved responses organized by ILPA section, with version control, an owner, and a last-reviewed date on each answer.

- Leverage a purpose-built AI tool. Manual workflows, generic AI, and horizontal RFP solutions don’t meet PE firms’ needs or scale with the growing volume of requests. Adopt an AI tool purpose-built for DDQs that enables the firm to maintain an up-to-date answer library, search and surface answers quickly, and collaborate across teams.

- Establish section-level ownership. The investment team owns strategy and valuation, operations owns risk and service providers, and compliance owns legal and regulatory. IR orchestrates as the single voice of the final document.

- Enforce consistency across artifacts. Discrepancies between the DDQ, the pitch deck, the data room, and verbal answers raise immediate red flags. Reconcile all of them whenever any one changes.

- Choose transparency over spin. Generic copy-paste answers invite deeper scrutiny. If a question does not apply, say why in one sentence, and address blemishes proactively.

- Treat speed as a signal. Delays read as disorganization. Set an internal SLA, roughly two to three weeks for a full fundraising DDQ, faster for monitoring updates.

For a deeper look at building this foundation, see How to improve the DDQ process.

Best practices that change by DDQ type

While the DDQ playbook is universal, the definition of a great answer is not. Each type of DDQ is read by a different audience that rewards a different kind of response.

Investment DDQs — narrative quality wins

The audience is the investment committee. Articulate the edge concretely; vague claims such as “we find great companies” get flagged. Make the track record reconcilable to the deck, and frame sensitive items as demonstrations of alignment rather than liabilities. The key prep move is to build the full ILPA DDQ 2.0 in advance of launching a fundraise, so the narrative is ready when diligence starts.

Operational DDQs — evidence wins

ODD reviewers want documentation, not prose. Maintain a standing evidence pack, including valuation policy, SOC reports, BCP test results, and org charts, and ensure answers align with actual practice, as ODD often includes an in-person or virtual walkthrough of a particular process. Log every answer: reviewers compare responses across years and notice what changed.

ESG DDQs — reliable data wins

The audience is ESG analysts, and requests are increasingly quantitative. Build the portfolio data pipeline once, aligned to EDCI definitions, and keep a single source of truth so the figure given to LP A in March matches the one given to LP B in June. Calibrate claims to evidence (greenwashing is a regulatory and reputational risk) and structure master answers around the PRI/ILPA question set since it covers most inbound variants.

Why purpose-built AI is the best way to manage every DDQ type

Traditional, manual DDQ workflows clearly can’t keep pace with the current volume PE firms receive. Answers live in old DDQs, email threads, and senior staff’s memories. Answer consistency degrades over time, and knowledge gaps widen as the volume of questionnaires grows across all three DDQ types.

Given advancements in LLMs, many PE firms have experimented with using a frontier model to respond to DDQs faster. However, generic LLMs can’t support DDQ best practices. Context window limits cap how much reference material can be processed at once — a full DDQ with supporting documentation can easily exceed those limits, forcing teams to truncate sources or break work into separate sessions where prior context is lost. There’s also no consistency: different team members prompting the same model independently can get materially different answers to the same question, and the same prompt can yield different outputs across sessions. Add to that no persistent answer bank, no citations to approved precedent, and no multi-stakeholder workflows, and the “upload and prompt illusion” creates false confidence in answers that were never vetted.

Learn more about the upload and prompt illusion.

Another option PE firms may consider is an AI-powered RFP solution. While it can store a content library, it doesn’t distinguish between fundraising, operational, and ESG questionnaires or fund strategies.

The advantages of purpose-built AI for DDQs

Ontra DDQ is built specifically for private markets fund managers. It digitizes incoming questionnaires, surfaces approved answers with AI taking the first pass, manages the workflow from intake to export, and builds the answer library in real time. Each capability maps back to a best practice above: the library becomes the answer bank, ownership becomes the review workflow, consistency becomes a single source of truth, and speed comes from the AI first pass.

For a closer look at the workflow, see How to automate DDQs with AI.

Stop drowning in DDQs

The playbook is universal; the execution is type-specific. The firms that field 100-plus questionnaires a year without burning out their IR teams are the ones that pair that discipline with purpose-built AI, whether they are a large-cap GP or an emerging manager facing a first institutional raise.