For CFOs and finance professionals at private equity firms, the growth of private credit isn’t just a headline. It’s a daily operational reality. Moody’s projects the broader private credit asset class could approach $4 trillion AUM by 2030, which coincides with a rising workload for private markets professionals.

Every new deal, every portfolio company acquisition, every capital call facility carries with it a credit agreement — a dense, legally binding document packed with covenants, reporting obligations, negative restrictions, and financial tests that must be tracked, monitored, and acted upon across the life of the investment.

As portfolios scale, the complexity compounds. And yet, many finance teams are still managing this reality with spreadsheets, shared drives, and manual review processes that were designed for a simpler time. The result is a growing gap between the operational demands of modern private credit and the infrastructure most firms have in place to manage it.

This guide is for PE finance teams that are ready to close that gap.

Two layers of credit: fund-level and asset-level

Finance teams operate across two distinct layers, each with its own logic, risk profile, and operational demands. Understanding these distinctions is essential to reviewing and implementing a credit agreement software solution.

Fund-level credit

At the fund level, the primary credit instrument is the subscription line of credit, often called a “sub-line” or capital call facility. Here, the borrower is the PE fund itself, not any of its portfolio companies. The lender’s collateral is the uncalled capital commitments of the fund’s limited partners, typically large institutional investors such as pension funds and endowments.

For PE finance teams, these agreements require careful tracking of borrowing base calculations, LP commitment data, and facility-level covenants. Fund-level agreements are also where back-office and finance teams do the most active benchmarking — reviewing what has been accepted in prior facilities to inform negotiations on new ones.

Asset-level credit

At the asset level, the picture is more complex. This is the traditional leveraged buyout (LBO) debt structure, where the borrower is the portfolio company itself. Collateral is the operating company’s assets — inventory, real estate, intellectual property, receivables. The debt is non-recourse to the fund, meaning a lender’s recovery in a default scenario is limited to the assets of that specific company.

Finance teams managing asset-level credit must track a wide range of credit facilities across dozens of portfolio companies simultaneously, each with its own lender, its own covenant package, and its own reporting and compliance calendar. This is where operational complexity reaches its peak — and where manual processes visibly break down.

How PE finance teams interact with credit agreements

The signing of a credit agreement isn’t the end of the finance team’s involvement; it’s the beginning. On any given week, the finance function may be engaged in all of the following activities simultaneously.

Covenant compliance monitoring

Affirmative and financial covenants require the borrower to maintain certain performance metrics, including Debt-to-EBITDA ratio, interest rate coverage ratio, or leverage ratio, to demonstrate compliance through periodic certificates delivered to the lender. Missing a delivery deadline or falling below a threshold can trigger a default.

Negative covenants limit a borrower’s actions by requiring lender consent for certain activities, while also defining specific permitted exceptions. They may prohibit additional indebtedness, restrict asset sales, or limit the payment of dividends. These restrictions become especially relevant when the firm is evaluating an add-on acquisition, refinancing a facility, or restructuring a portfolio company’s balance sheet. The job-to-be-done here is not just monitoring — it is proactively understanding restrictions across all active facilities before a strategic decision is made.

Reporting package preparation

In private credit deals, lenders demand a level of financial and liquidity transparency that far exceeds the reporting provided to LPs. Finance teams are typically obligated to deliver audited financial statements, detailed budget-versus-actual analyses, and written disclosure of any material adverse developments. The cadence, format, and content of these packages are all governed by the credit agreement — and non-compliance with reporting requirements can itself constitute a default.

Cash flow waterfall management

The credit agreement defines the order in which cash generated by the business must be distributed. Before any dividends can flow to the PE sponsor or its limited partners, interest payments, principal amortization, and reserve requirements must be satisfied. Finance teams are responsible for ensuring these waterfall mechanics are followed precisely, particularly as liquidity conditions evolve.

Amendment and waiver negotiations

Strategic activity — an add-on acquisition, an asset sale, a refinancing — frequently requires the finance team to return to the lender and seek an amendment or waiver. This process requires a deep understanding of what the current agreement permits and prohibits, what precedent was set in prior negotiations, and what the lender’s likely threshold for approval will be.

Borrowing costs

Most private credit facilities price off a floating benchmark rate — typically SOFR — plus a negotiated credit spread that may step up or down based on a leverage pricing grid. To model the true all-in cost of debt, finance teams need the applicable margin and pricing grid, any benchmark rate floors, and the full fee schedule, including OID, unused commitment fees, and agency fees. These inputs shift as financial performance changes, making accurate, up-to-date access to credit agreement terms essential.

Each of these activities demands accurate, accessible, and current information from the credit agreements themselves. That is exactly what manual systems fail to provide at scale.

Why manual credit agreement management is failing PE finance teams

Lack of historical context

One of the most persistent pain points for deal teams and finance professionals alike is the inability to quickly access what was agreed to in prior transactions. When negotiating a new credit facility or a complex amendment, the ability to benchmark proposed terms against historical precedent is a significant source of leverage.

- Which lenders have previously accepted maintenance covenant packages?

- What was the last agreed EBITDA add-back definition?

- What restricted payment baskets have been negotiated in comparable deals?

This information almost always exists somewhere in the firm’s records. The problem is finding it — and finding it quickly enough to be useful. In a manual environment, that search can take days of lawyer review, email chains across multiple deal teams, and excavation of shared drives organized by someone who may have left the firm years ago.

Finance and back-office teams can end up negotiating without the full benefit of their own institutional knowledge, moving from reactive searching to proactive benchmarking only when a better system is in place.

Covenant compliance tightrope

Tracking covenant compliance across a large portfolio requires continuous, simultaneous attention to multiple moving variables: financial tests calculated on different cadences, compliance certificates with different delivery deadlines, and lender-specific definitions of key financial metrics that may vary from one agreement to the next.

At small portfolio sizes, a disciplined spreadsheet process managed by a capable analyst may be sufficient. As a fund scales — and as the number of active credit facilities grows — the margin for human error expands accordingly. A missed covenant calculation, a delayed compliance certificate, or a misread definition can trigger a technical default, initiating a lender notification process that is expensive, disruptive, and reputationally damaging, even when the underlying business is performing well.

The cost of over-reliance on external counsel compounds this problem further. Finance teams lacking organized access to credit agreements frequently escalate routine questions to outside counsel. This is particularly common regarding permitted activities and lender consent requirements, as teams often struggle to efficiently locate or parse the necessary provisions internally. This back-and-forth represents a significant and largely avoidable expense for questions that a well-configured internal system should answer in seconds.

Version control problems

Credit agreements are amended frequently. Facilities are restated, extended, and modified throughout the life of the investment. In a manual environment, tracking which version of an agreement is operative — and whether all amendments have been properly integrated — is a persistent source of risk. Finance teams may act on outdated terms or fail to enforce provisions added in a subsequent amendment that was never properly filed alongside the original.

What to look for in credit agreement management software

Generic document management platforms and basic OCR tools lack the domain-specific intelligence PE finance teams require. When evaluating purpose-built software, the following capabilities should anchor the assessment.

Contract digitization and structured data extraction

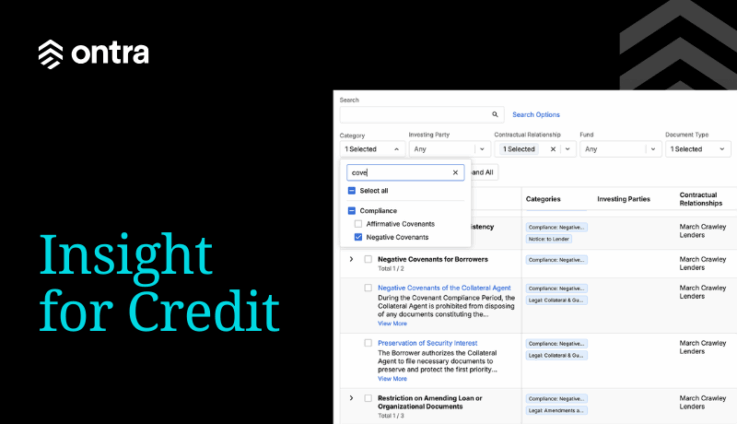

The foundation of any credit management system is the ability to transform dense, unstructured credit agreement documents into clean, structured, searchable data. The software should extract key covenants and organize them in a consistent format that enables cross-portfolio comparison.

Covenant abstraction and categorization

AI-powered abstraction tools can identify covenant types, flag obligations with upcoming deadlines, and surface potential conflicts between proposed actions and existing agreement restrictions — without requiring a lawyer to read every page. This capability is particularly valuable for finance teams managing a large and growing portfolio where manual review can’t keep pace.

Side-by-side term comparison

The ability to compare terms across multiple credit agreements in a single view is one of the highest-value capabilities a finance team can access. Whether benchmarking proposed lender terms against historical precedent, comparing covenant packages across portfolio companies, or identifying which facilities contain provisions that may conflict with a contemplated transaction, this functionality transforms institutional knowledge into an active competitive advantage.

Proactive obligation tracking and alerts

Purpose-built software converts the obligations embedded in credit agreements into structured tasks with automated alerts, escalation workflows, and audit trails. Teams should be notified of upcoming compliance certificate deadlines, financial test calculation dates, and lender reporting requirements well in advance — not after a deadline has passed.

Robust data security and access controls

The software solution should meet institutional-grade security standards, including encryption at rest and in transit, role-based access controls, and comprehensive audit logging. For firms managing fund structures across multiple jurisdictions, configuring data residency and access permissions at the entity level is an important consideration. Verify SOC 2 compliance and understand the vendor’s data handling practices before committing.

Top benefits of credit agreement management software

The business case for purpose-built credit agreement management software extends well beyond avoiding compliance failures — though that alone is substantial. Finance teams that move from reactive document management to proactive, data-driven credit oversight unlock several distinct sources of value.

Time savings at scale

The hours finance and legal teams spend searching for, reviewing, and interpreting credit agreement provisions represent one of the largest sources of recoverable time in the back office. When the answer to “what does our revolving credit agreement say about permitted acquisitions?” is available in seconds rather than days, the finance team is free to spend its time on analysis and decision support.

Risk reduction through visibility

Firms that lack a complete, current view of their covenant exposure across all active facilities are operating with a blind spot that typically surfaces at the worst possible moment. A unified platform that surfaces covenant status, upcoming obligations, and potential default triggers in real time eliminates this blind spot and gives the CFO confidence that the firm is not one missed calculation away from a technical default.

Negotiating leverage through institutional memory

Finance teams with organized access to historical deal terms negotiate from a position of strength. When a lender proposes a covenant package more restrictive than what the firm has historically accepted, the ability to produce a benchmarking analysis quickly is a meaningful advantage. Understanding the full range of terms previously negotiated enables the deal team to push harder on issues that matter most.

Scalability without headcount growth

As private credit continues to expand and deal volumes increase, the operational burden of manual credit agreement management will scale linearly with portfolio size — unless firms invest in automation. Purpose-built technology creates a fundamentally different relationship between portfolio complexity and operational cost, allowing finance teams to manage more credit facilities without a proportional increase in staff.

Prepare your finance team for the next stage of growth with Ontra

The private credit market will continue its expansion — AUM is expected to approach $4 trillion by 2030, with investing shifting toward asset-backed finance and growing momentum in international markets. For PE finance teams, this trajectory means more credit agreements to manage, more covenants to monitor, and more reporting obligations to fulfill.

The firms best positioned to scale into this environment are those that treat their credit agreement infrastructure as a strategic asset rather than an administrative burden. That means moving away from spreadsheets and shared drives toward purpose-built technology that digitizes credit agreements, automates compliance workflows, and converts institutional knowledge into an accessible, searchable database.

For CFOs evaluating credit agreement management software, the question is not whether the investment in better tooling is justified. The volume and complexity of credit activity in today’s market make that answer clear. The more relevant question is how quickly the firm can onboard a solution and how much operational risk it is willing to carry in the meantime.

The best credit agreement management platforms give finance teams something no spreadsheet can: Answers that are organized, accessible, and accurate. In a market where the margin for error is tightening, and the cost of a compliance failure is higher than ever, that confidence isn’t a luxury. It’s a competitive requirement.